We’re all much more focused on how much we’re spending when we buy, and money has suddenly come sharply into focus.

But how much thought do you give to the value of your money? And how its value could affect your longer-term banking products like investments, mortgages, and (third).

If you’re based in Europe, like a lot of Monefit users, you’ll likely have at least heard the term Euribor. But do you know much about it? What it is, how it works, and how it could affect you and the value of your money?

If not, and you’re curious, you’ve hit the jackpot. Here is our Monefit guide to the basics of the Euribor.

What is it?

Firstly, Euribor is an acronym, or shortening, of the Euro Interbank Offered Rate.

This is an overnight interbank rate made up of the average interest rates from a panel of large European banks that are used for lending to one another in euros.

It is sometimes referred to as “the price of money” as it effectively sets the rate at which banks lend to each other to maintain liquidity and meet reserve requirements.

There are also five different maturities of the Euribor – one week, one month, three months, six months, and 12 months.

How is it calculated?

The European Money Markets Institute requests interest rates daily from each of the banks in the euro zone. Specifically, they ask at 10:45, to publish the rate at 11 CET. Participating banks then submit the rate at which they are willing to borrow or lend funds all five maturities.

They then calculate the Euribor by eliminating the highest 15% and the lowest 15% of the interest rates submitted and calculating the arithmetic mean of the remaining values.

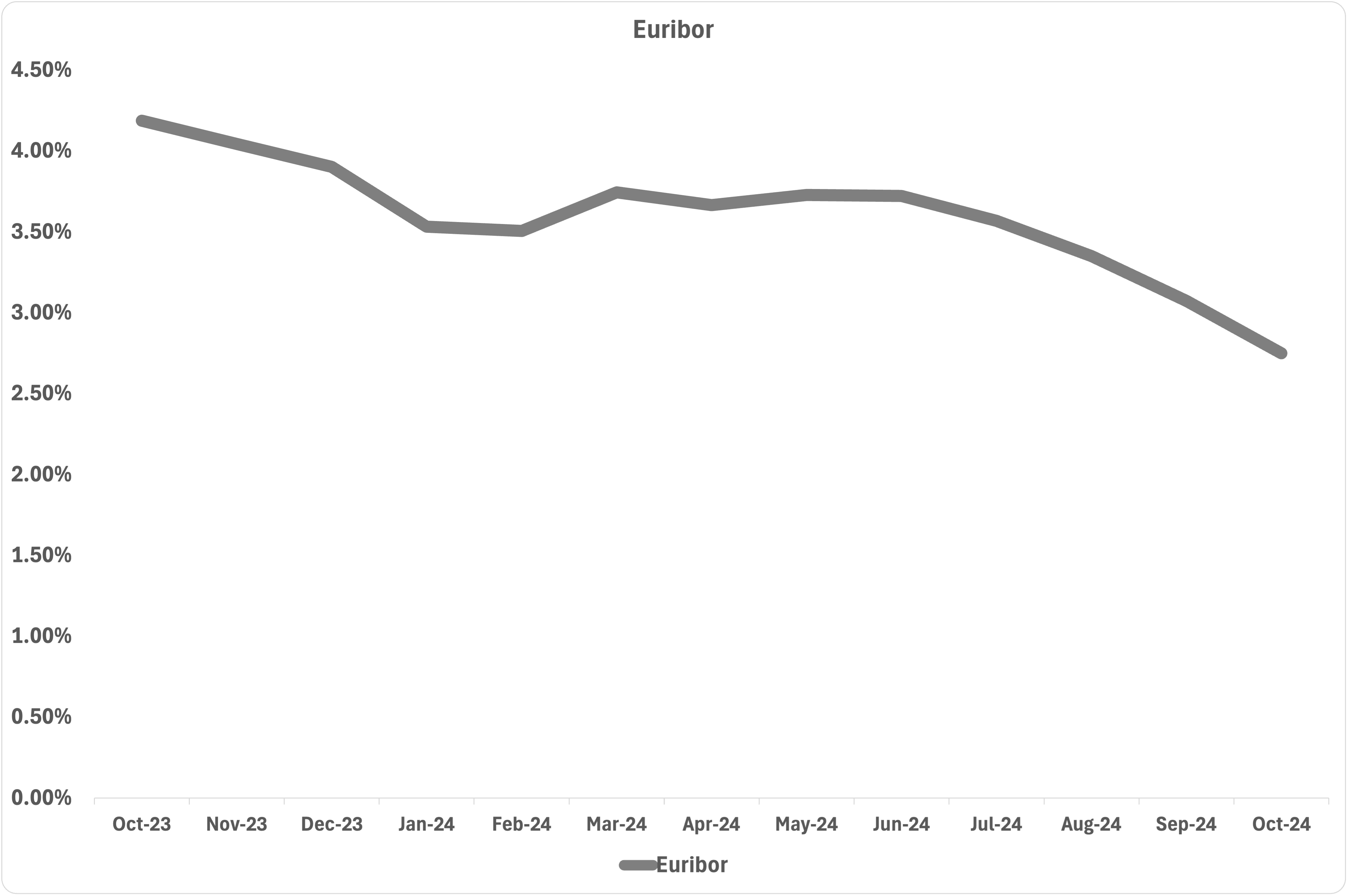

Euribor 1 week rate, last 6 months, taken from https://www.euribor-rates.eu/

External factors like supply and demand, economic growth, and inflation influence the level of the rates submitted by each bank.

What does it affect?

The first major financial product for individuals to consider when thinking about the Euribor is their mortgage.

The majority of mortgages in mainland Europe offer a fixed interest rate which is then added to the six-month Euribor rate. This then dictates your monthly mortgage payment, meaning a higher Euribor makes your monthly bills grow, while a falling Euribor is kinder to your wallet.

The next thing to look at is your savings account. While the Euribor doesn’t directly affect your savings, if the Euribor rate is not favourable to banks and decreases their overall earnings, they’re more likely to then lower rates across the board. This includes in your savings account.

Finally, if you’re a seasoned investor, the movement of the Euribor will likely offer insights into the wider risk appetite of banks and the strength of the Euro as a currency.

Are there other rates to consider next to the Euribor?

In Europe, the rate that has a heavy impact on the Euribor is the European Central Bank (ECB) rate.

While it has no direct bearing on the Euribor, the ECB’s monetary policy is to influence liquidity on the interbank market (and therefore the Euribor rates) through its various operations and tools (one of them being the ECB interest rates).

Outside of Europe, the London Interbank Offered Rate, or LIBOR, is critical for the UK and US financial markets and a topic we’ll visit again in the near future.

What about Monefit’s rates?

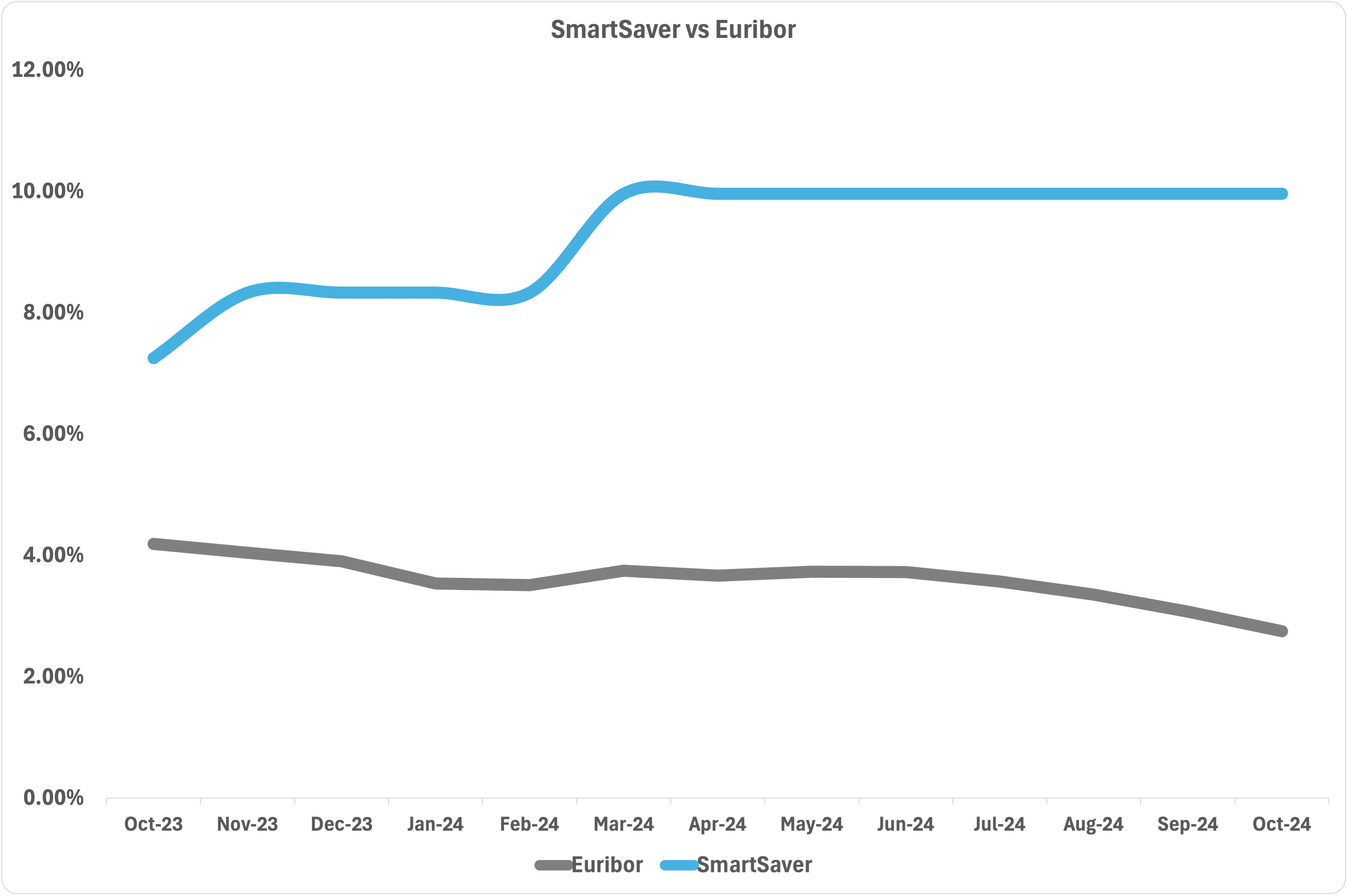

So how does this all compare to the rates you’ll get with Monefit’s key investment product SmartSaver?

Since SmarSaver launched in 2022, our rates have only gone up, with our base SmartSaver rate of 7.25% APY staying steadfast, while our fixed-term Vaults offer 8.87% APY and 9.96% APY.

And none of it is affected by the Euribor. So why not start saving with us, and a rate that won’t be moving around daily?

And none of it is affected by the Euribor. So why not start saving with us, and a rate that won’t be moving around daily?

Get started with SmartSaver today, and start living your best financial life.

*The information presented in this blog post is valid as of the time it is published. The content is intended to provide information only and is not meant and should not be considered as financial or investment advice of any kind.